Most incentive management software wasn’t built for financial services. The platforms that dominate e-commerce and DTC software guides assume quick transactions, instant reward delivery, and no regulatory complexity. Banking doesn’t work that way.

This guide is for marketing and growth leaders at banks, credit unions, and fintechs evaluating software to handle their incentive and offer programs, from referrals to welcome offers to product upgrade incentives. It covers the compliance requirements that shape every program decision, the fraud risks specific to financial products, key banking integrations to consider, and what to ask any vendor before you sign.

Why Referral and Rewards Programs Work Especially Well for Banks and Credit Unions

Financial products are high-trust decisions. A consumer doesn’t open a new checking account because of a banner ad — they do it because a friend recommended the institution, because a family member is already a member and loves it, or because a colleague mentioned the rate was worth switching for. That word-of-mouth already happens organically at every bank and credit union. A referral program formalizes it, attributes it, and rewards it.

The financial services context makes referred customers especially valuable:

- Referred customers have a 16% higher lifetime value and 18% lower churn rate than non-referred customers

- Finserv customer acquisitions by referral cost 50% less than the average finserv customer acquisition.

- 93% of consumers trust a recommendation from a friend or family member, compared to 38% who trust a brand advertisement

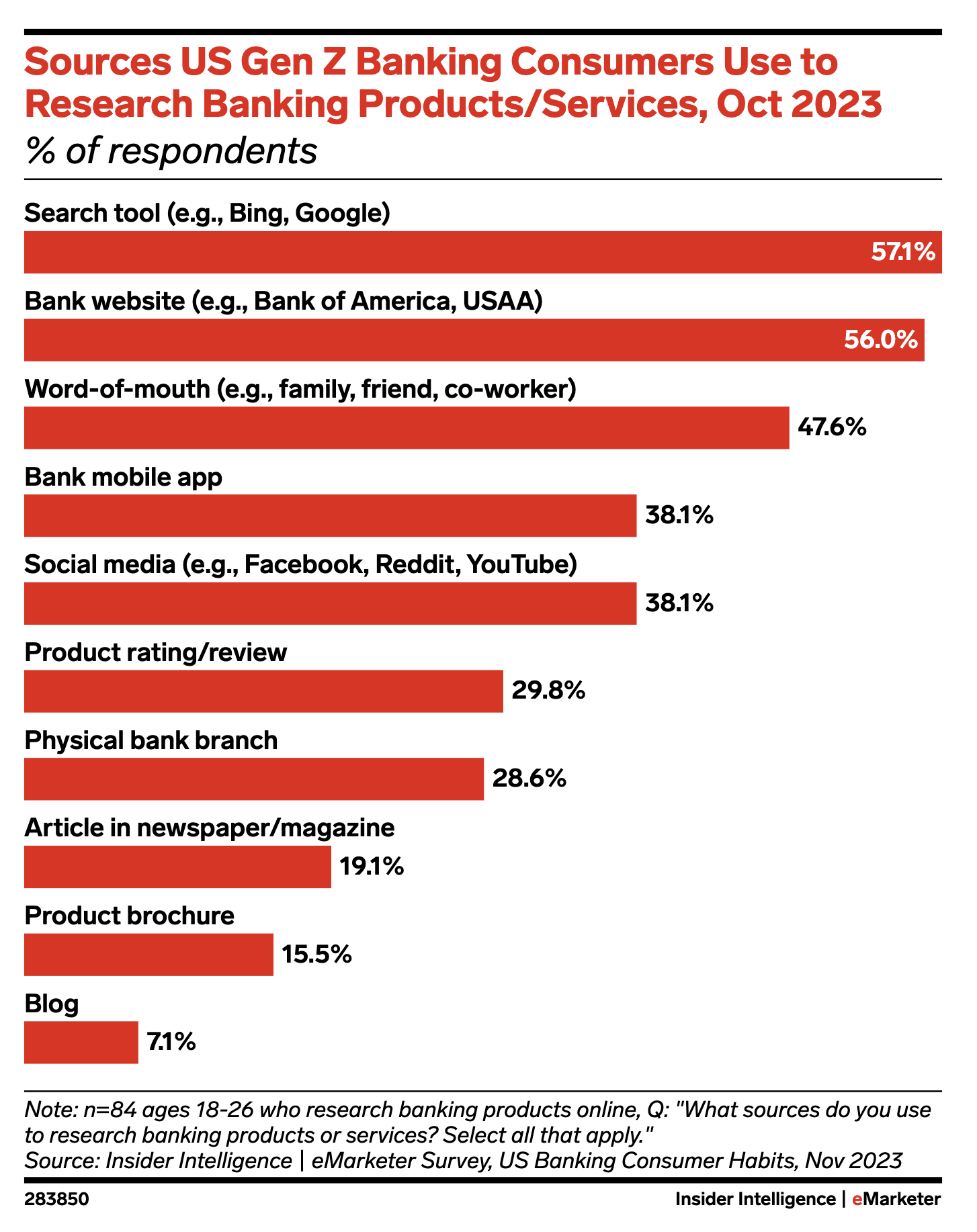

- Looking for a younger demographic? 47.6% of Gen Z places word-of-mouth referrals as a top-three priority when choosing a banking product or service

- Referred customers are more likely to open additional products and cross-sell into deeper relationships

The key to leveraging this powerful growth strategy is choosing the right incentive management software to power it. This guide is a great place to start.

In This Article

-

-

-

- The Compliance Landscape for Incentive Programs in Financial Services

- Incentive Program Fraud Risks Specific to Banks and Credit Unions

- How Extole Manages Incentive Programs in a Regulated Environment

- Referral Program Design for Banks and Credit Unions

- Key Integrations Financial Institutions Should Consider

- Questions to Ask Any Referral Vendor Before Signing

- Conclusion

- FAQ

- The Compliance Landscape for Incentive Programs in Financial Services

-

-

The Compliance Landscape for Incentive Programs in Financial Services

Compliance is where the financial services industry diverges most sharply from other industries. Every incentive program decision — what rewards to offer, how to describe them, when to issue them, how to communicate about them — happens inside a regulatory framework that doesn’t apply to retail or DTC. Here’s what that means in practice:

UDAAP: Every Customer-Facing Word Matters

The prohibition on Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) applies directly to how your referral program is presented. The reward description, the eligibility terms, and the conditions for earning have to be clear, accurate, and non-misleading.

What to look for in an incentive management platform:

- Full control over all customer-facing copy

- Required disclosures displayed automatically wherever referral, reward program, or sweepstakes content appears

- Compliance without disruption: customer experiences are still seamless and on-brand

BSA/AML: Cash Rewards Require a Paper Trail

When a referral program pays a cash bonus for bringing in a new account holder, that payment is the kind of transaction that Bank Secrecy Act and anti-money laundering controls are designed to document. Every reward transaction needs to be fully logged: who referred whom, what qualifying event triggered the reward, when it was issued, and to what account. This documentation is required to satisfy an audit or respond to a regulatory examination.

What to look for in an incentive management platform:

- Complete, immutable audit trails for every referral event and reward state change

- Teams with a comprehensive understanding of relevant BSA/AML regulations

NCUA Regulations for Credit Unions

Credit unions are subject to National Credit Union Administration oversight, which governs how member inducements can be structured and communicated. Referral rewards paid to existing members for bringing in new members need to be consistent with NCUA guidance on member incentives. The program’s terms and conditions must also satisfy Truth in Savings Act (TISA) disclosure requirements — meaning that if a referral reward is tied to a deposit account in any way, the offer has to be described accurately and disclosed properly.

What to look for:

- ISO 27001 certification

- Information security policies consistent with NCUA standards

- Comprehensive audit trails and thorough documentation

- Automatic referral reward disclosure in compliance with TISA requirements

- Teams with deep experience in financial services, particularly in the credit intermediation sector

Platforms without specific experience running credit union referral programs will require significant customization to operate safely within NCUA and TISA requirements.

1099 Reporting and Tax Compliance

There are separate qualifications for taxable rewards in financial services depending on the value of the reward and how it is earned. Cash rewards for completing a “service” like referring a friend are only taxed when they exceed applicable IRS thresholds (currently $1200). These require 1099-MISC reporting.

Other rewards are treated as “interest” rather than rewards—account bonuses such as welcome offers fall into this category. These need to be reported on a 1099-INT form when they exceed $10.

What to look for:

- Automated tracking of cumulative reward values per individual

- All necessary tax documentation available to your institution and/or customers when relevant

- Control over reward thresholds to prevent customers from unknowingly exceeding untaxed reward limits

- Teams with up-to-date knowledge of relevant tax regulations

TCPA and CAN-SPAM

Referral programs involve outbound communication: advocates share referral links via email or SMS, and programs send reward notifications and follow-up messages to referral participants. Every piece of that communication is subject to TCPA regulations for text/SMS and CAN-SPAM for email.

What to look for:

- Support for proper consent capture before any outbound communication

- Visibility and control over all outbound messaging for your compliance team

- Email templates pre-built for CAN-SPAM compliance

- Ability to opt-out customers at their request (automatically or via manual upload)

- Transparency regarding any additional permissions your program may need

GDPR and CCPA

Institutions with customers or members covered by GDPR need a referral platform that functions as a compliant data processor. CCPA applies to California residents regardless of where your institution is headquartered.

What to look for:

- Configurable consent checkboxes embedded in share experiences

- Cookie consent integration

- APIs for real-time retrieval of any data subject’s profile, including events, relationships, device ID, etc.

- Ability to directly update or correct profile and relationship data

- Certifications under the E.U.-U.S. Data Privacy Framework

Incentive Program Fraud Risks Specific to Banks and Credit Unions

Referral fraud in financial services is not the same problem as referral fraud in retail. The attack patterns are more sophisticated, the fraud economics are more attractive, and the regulatory exposure from inadequate controls adds risk well beyond wasted reward budget.

Synthetic Identity Fraud

When cash rewards are offered for new account openings, bad actors can sometimes exploit program gaps to manufacture the qualifying event using synthetic or borrowed identities. This is one of the most significant fraud vectors in financial services referral programs — and it requires controls at the identity verification layer, not just the reward layer. The reward should only be issued after KYC is completed and verified, not after an account is opened.

Self-Referral and Duplicate Account Fraud

More common and lower-stakes: customers creating multiple accounts to collect both sides of a two-sided referral reward. Device fingerprinting and browser-level identification are the primary defenses. A browser identifier tied to a device — not just an email address — creates a signal that persists even when a bad actor rotates email addresses.

Referral Farming

Rarer but high-consequence, this refers to organized fraud rings exploiting referral bonuses through coordinated programs using networks of real or synthetic accounts. IP-based anomaly detection and velocity controls are necessary to catch the patterns that individual account checks miss.

Exploiting Pending Reward States

Financial referral programs involve complex reward conditions — reward only after KYC passes, after a minimum deposit, after direct deposit is received, after a debit card transaction. Programs with weak controls around reward state management can be exploited when bad actors understand the conditions and manufacture qualifying events without genuine customer intent.

How Extole Manages Incentive Programs in a Regulated Environment

Event-Based Reward Triggers Tied to Real Banking Events

The single most important capability difference between general-purpose incentive management software and platforms built for financial services is event-based reward logic. In retail, a reward fires when someone makes a purchase. In financial services, the qualifying event is almost always downstream: minimum deposit received, KYC verification passed, direct deposit received, debit card activated, first transaction completed, loan funded.

Extole supports complex reward rules and pending-state rewards for exactly this reason: rewards are applied only when every triggering condition is confirmed within the specified time period. Extole’s Reward Bank feature also allows offer stacking (for example, a monthly account credit applied for the first six months after a referral) in addition to one-time payouts.

Core Banking Integration

A referral platform that can’t talk to your core banking system creates manual reconciliation work at every step. Extole supports native integration with FIS, Fiserv, Candescent, Jack Henry, and Q2 — the major core banking platforms used by banks and credit unions in the U.S. This integration is what enables reward triggers to fire on actual banking events, not just front-end interactions, and what allows referral data to be reconciled against real account activity.

Manual Review Gates for High-Value Rewards

Automated fraud detection catches most bad actors. Manual review gates catch the rest and give your compliance team a control point before any reward is disbursed. Extole supports configurable approval workflows that can hold rewards for review, flag specific transactions for compliance inspection, or require manual sign-off before any cash reward is paid.

Multi-Layer Fraud Detection

A well-built platform for financial services uses multiple signals simultaneously:

Browser-level identification. Extole assigns a persistent browser identifier (xtl_bid) to each program participant. When the same device cycles through multiple email addresses, that pattern is visible and flagged — even when each individual account appears legitimate on its own.

IP and geolocation intelligence. Extole integrates with MaxMind’s GeoIP database and minFraud services, evaluating every program interaction against IP-based risk signals: proxy usage, VPN activity, high-velocity requests from a single IP, and geographic anomalies that don’t match account information.

Consumer verification tiers. Extole uses a three-tier identity model. An anonymous user can view program creatives but cannot share. An identified user (email provided) can share but cannot access any PII. A verified user has proven their identity and has access to their own program history and rewards. Sensitive data — friend emails, conversion history — is never accessible without verification.

KYC integration hooks. Extole supports integration with identity verification systems so reward triggers can be conditioned on KYC completion, not just account opening. Rewards stay in a pending state until the KYC event is confirmed by your systems.

Comprehensive Audit Trails

Every referral event, every reward state change, every manual review action needs to be logged in a complete, immutable record. For financial institutions, this is the documentation required to respond to regulatory examination, internal audit, or a customer dispute. Extole maintains complete audit trails automatically — no custom engineering required to produce the records your compliance team needs.

Complete Data Subject Rights Support

When your institution receives a data subject access request, correction request, or erasure request, your referral platform has to be able to respond. Extole supports the full suite:

- Right to Access: Real-time API retrieval of any data subject’s complete profile — referral events, quality scores, advocate and friend relationships, device and IP data, customer journey information. Queryable by email, retrievable by your team on demand.

- Right to Correction: Most profile and relationship data is updatable via API. Historical event corrections can be handled through Extole’s support team.

- Right to Erasure: Requests submitted via email or API trigger irreversible pseudoanonymization — the profile is severed from the individual within seven days of the request.

Disclosure Management

Extole supports automated disclosure management so required legal language can be systematically appended to program touchpoints, including advocate-shared messages, friend landing pages, and reward confirmations. Your compliance team can configure required disclosures once and have them appear consistently without manual review of individual shares.

ISO 27001 Certification

ISO 27001 is often a vendor prerequisite that financial institutions require before security review even begins. Extole is ISO 27001 certified, independently audited through BSI and accredited by the ANSI National Accreditation Board. This covers the full scope of how Extole’s systems are built and maintained — physical security, software development, data handling, HR processes, and management oversight.

Referral Program Design for Banks and Credit Unions

What Rewards Actually Work for Financial Products

The right incentive structure varies by product and institution type:

For checking and savings account referrals: Cash bonuses are the most effective incentive — both for the advocate and the referred friend. Two-sided rewards (a bonus for both parties) consistently outperform one-sided rewards. Typical ranges run $50–$200 per completed referral depending on the product.

For credit unions: Account credits, rate discounts on loans, and waived fees are well-suited to the member relationship and align with NCUA guidance on member inducements. Charitable donation options are also popular with credit union member bases.

For credit card referrals: Statement credits and points bonuses are natural fits that align with the product itself. Cash back rewards also perform well.

For loan products: Because loan approval involves a longer process, reward triggers typically need to be tied to funding events rather than application submission — which requires the event-based trigger infrastructure described above.

Member-to-Member vs. Employee-to-Member Programs

Financial institutions often run two distinct referral models simultaneously:

Member-to-member (or customer-to-customer) referrals are the classic refer-a-friend program: existing members share a personalized referral link via email, text, or social media, and earn a reward when the friend opens an account or takes a qualifying action.

Employee-to-member referrals — sometimes called staff referral programs — give branch staff, loan officers, and relationship managers the ability to capture referrals directly and track their performance. This is particularly valuable for community banks and credit unions where personal relationships drive a significant share of new accounts. Extole’s Go Extole mobile app gives field teams and branch staff the ability to capture referrals in person by scanning a QR code or submitting a referral directly from their phone. This makes it simple to track and attribute in-person advocacy the same way digital referrals are.

Omnichannel Attribution: Bridging Digital and In-Branch

A member might hear about a program in a branch visit, go home and apply online, and complete KYC three days later. A referred friend might click a digital referral link but ultimately open their account at a branch. Your referral platform needs to bridge those touchpoints and ensure the advocate gets credit regardless of which channel the conversion happens in.

Extole tracks referral events across web, mobile app, in-branch, and offline channels — and bridges digital and physical so that attribution is accurate even when the conversion journey spans multiple channels over multiple days.

Key Integrations Financial Institutions Should Consider

Core banking systems: FIS, Fiserv, Candescent, Jack Henry, Q2 — native integrations that allow reward triggers to fire on real banking events.

CRM: Salesforce and HubSpot two-way sync, so referral events are visible alongside the rest of your customer data. Essential for institutions with longer member lifecycle journeys and relationship-driven acquisition.

Email and SMS platforms: Integration with Klaviyo, Attentive, and other marketing automation platforms ensures referral communications are consistent with your broader member communications and that consent is managed through your existing infrastructure.

Digital banking platforms: For digital-first banks and fintechs, embedded referral experiences within your mobile app or online banking portal are achievable through Extole’s mobile SDKs (iOS, Android, and React Native) and API-first architecture.

Questions to Ask Any Referral Vendor Before Signing

- Can your platform hold rewards in a pending state until specific banking events are confirmed — KYC completion, minimum deposit, direct deposit receipt, debit card activation?

- Do you support manual review gates before any cash reward is disbursed?

- What specific fraud detection mechanisms are active by default for financial services programs?

- Do you support in-branch and offline referral capture for employee and relationship manager programs?

- What audit trail documentation do you provide, and in what format?

- How do you handle data subject access, correction, and erasure requests under GDPR and CCPA?

- Are you ISO 27001 certified? Do you have a Data Processing Agreement available?

- Which core banking platforms do you integrate with natively?

- Do you support 1099 reporting and tax compliance for high-value rewards?

- Do you support automated disclosure management for UDAAP and TISA compliance?

- What experience do you have running referral programs specifically for banks and credit unions — and can you share client references in this vertical?

The Bottom Line

Referral programs work exceptionally well for banks and credit unions. The trust dynamics of financial relationships make word-of-mouth one of the highest-converting acquisition channels available — and referred members consistently outperform non-referred members on retention, lifetime value, and product depth.

What doesn’t work is running those programs on platforms that weren’t built for regulated environments. The compliance requirements are real. The fraud vectors are different. The integration needs are more complex. And the audit expectations don’t leave room for gaps.

The right referral platform for a bank or credit union treats compliance controls, fraud prevention, core banking integration, and audit infrastructure as default capabilities — not add-ons you negotiate for. If you’re evaluating referral software for a financial institution and want to talk through what that looks like in practice, schedule a demo with Extole’s financial services team.

Frequently Asked Questions About Incentive Management Software for Banks and Credit Unions

Financial institutions evaluating incentive management software often need answers about

compliance, fraud prevention, integrations, auditability, and referral program design. These

FAQs cover the most common questions banks, credit unions, and fintech teams ask when

comparing referral and incentive platforms for regulated environments.

What is incentive management software for banks and credit unions?

Incentive management software for financial institutions is technology that helps banks,

credit unions, and fintechs launch, track, and optimize programs such as referral programs,

welcome offers, account-opening bonuses, product upgrade incentives, and employee referral

initiatives. Unlike generic referral software, financial services incentive platforms must also

support regulatory compliance, fraud prevention, audit trails, and integrations with core

banking systems.

Why do banks and credit unions need specialized referral or incentive management software?

Banks and credit unions operate in a regulated environment where reward timing,

disclosures, eligibility requirements, tax reporting, and customer communications all matter.

Specialized software is needed because financial products often require rewards to be

triggered only after downstream events such as KYC verification, minimum deposit,

direct deposit setup, debit card activation, or loan funding. Generic ecommerce referral

tools usually are not designed for these requirements.

What compliance requirements should financial institutions consider for incentive programs?

Financial institutions should evaluate incentive software against multiple compliance

requirements, including UDAAP, BSA/AML controls, NCUA guidance for credit unions,

Truth in Savings Act disclosure obligations, 1099 reporting requirements, TCPA, CAN-SPAM,

GDPR, and CCPA. The best platforms support configurable disclosures, consent capture,

detailed logging, tax-related reward tracking, and data subject rights workflows.

How does UDAAP affect referral and incentive programs in financial services?

UDAAP affects how referral and incentive offers are presented to consumers. Reward

descriptions, eligibility criteria, and terms must be clear, accurate, and not misleading.

A strong incentive management platform should give compliance teams control over

customer-facing copy and automatically display required disclosures across referral and

reward touchpoints.

Why are audit trails important in banking referral software?

Audit trails are essential because financial institutions may need to prove who referred whom,

what qualifying event triggered a reward, when the reward changed status, and whether a

manual review occurred before payment. Complete, immutable audit logs support internal

audits, regulatory examinations, customer dispute resolution, and compliance review.

What fraud risks are unique to financial referral programs?

Financial referral programs face fraud risks that go beyond standard ecommerce abuse.

Common risks include synthetic identity fraud, self-referrals, duplicate account fraud,

referral farming, and manipulation of pending reward conditions. Because financial rewards

may be tied to account openings or funding events, institutions need stronger controls than

simple email-based validation.

What fraud prevention features should banks look for in referral software?

Banks and credit unions should look for multiple layers of fraud detection, including device

or browser identification, IP intelligence, geolocation analysis, velocity controls, manual

review gates, and the ability to hold rewards in a pending state until qualifying banking

events are confirmed. Platforms that can connect reward eligibility to KYC completion are

especially valuable in regulated environments.

Can referral rewards be delayed until banking events are completed?

Yes. In financial services, rewards often should not be issued immediately after a referral

click or account application. Instead, they may need to remain pending until events such as

identity verification, minimum deposit, direct deposit receipt, debit card activation, first

transaction, or loan funding are confirmed. Event-based reward logic is one of the most

important capabilities to evaluate in financial incentive software.

What integrations matter most for incentive management software in banking?

The most important integrations usually include core banking systems, CRM platforms, email

and SMS tools, and digital banking experiences. Core banking integrations matter because

they allow referral rewards to be tied to real account activity instead of only front-end actions.

CRM and communications integrations help keep referral activity visible within the broader

customer journey and ensure messaging stays consistent with consent and compliance rules.

Do credit unions have different referral program requirements than banks?

Yes. Credit unions may need to align referral incentives with NCUA guidance on member

inducements and ensure that any deposit-related offers are disclosed in a way that supports

Truth in Savings Act requirements. Credit unions should also assess whether the vendor has

real experience operating referral programs in the credit intermediation sector.

How does tax reporting work for referral rewards in financial services?

Tax treatment depends on how the reward is earned and the value of the reward. Some

referral rewards may require 1099-MISC reporting, while some account bonuses may be

treated as interest and reported on a 1099-INT. Incentive platforms should help institutions

track cumulative reward values, manage thresholds, and support access to the documentation

needed for tax compliance.

Can banks and credit unions run both customer and employee referral programs?

Yes. Many financial institutions operate both customer-to-customer referral programs and

employee-to-customer referral programs at the same time. This can be especially useful for

community banks and credit unions where branch staff, loan officers, and relationship managers

influence acquisition. The right platform should support digital, in-person, and offline referral capture.

What makes a referral platform suitable for a regulated environment?

A referral platform is better suited for regulated industries when compliance controls, fraud

prevention, event-based reward triggers, disclosure management, audit logs, manual review

workflows, privacy rights support, and security certifications are built into the product rather

than treated as custom add-ons. For banks and credit unions, these capabilities are operational

requirements, not nice-to-have features.

What questions should financial institutions ask an incentive management software provider?

Financial institutions should ask whether the platform can hold rewards pending until banking

events are confirmed, support manual review before cash payouts, document every reward

state change, provide strong fraud controls, support in-branch attribution, integrate with core

banking systems, automate disclosure management, and help with privacy and tax compliance.

Vendor experience serving banks and credit unions is also an important evaluation criterion.