Top 10 Referral Program Examples in Financial Services Today

Financial services companies face a persistent challenge: acquiring customers in an industry where trust is everything and advertising costs keep climbing. Finserv referral programs solve both problems by turning satisfied customers into advocates who bring in friends and family—people who arrive already trusting your brand.

The most successful fintechs and banks have built referral programs that drive significant growth while keeping acquisition costs well below paid channels. This guide breaks down ten real examples from companies like Chime, Robinhood, and Coinbase, along with the specific tactics that make their programs work.

What is a financial services referral program

Financial services referral programs reward existing customers for bringing in new ones, typically through mutual cash bonuses, gift cards, or account perks. Top examples include Chime ($100), Robinhood (free stock), SoFi (cash bonuses), and Coinbase (cryptocurrency rewards). The model works across the entire financial industry—traditional banks, credit unions, fintechs, and investment platforms all use referral programs to acquire new users while engaging their existing ones.

The basic structure involves four components:

- First, there’s the advocate—the existing customer who shares a unique link or code.

- Next, there’s the referred friend who opens an account using that link.

- An incentive structure determines what rewards go to one or both parties and when.

- Finally, an events tracking system attributes referrals, verifies qualifying actions, and triggers reward fulfillment automatically.

What makes referral programs particularly powerful in financial services is the trust factor. When someone recommends a bank or investment app, they’re vouching for where you put your money. Nielsen research shows 88% of consumers trust personal recommendations more than any other channel.

Why referral programs drive growth for banks and fintechs

Trust is everything when it comes to money. According to research from the Wharton School, referred customers are 18% more likely to stay with a company than customers acquired through other channels. That loyalty translates directly into higher lifetime value and lower churn—metrics that matter enormously when customer acquisition costs in financial services reach $2,167 to $4,056 per customer.

Beyond trust, referral programs offer several distinct advantages:

- Lower acquisition costs: Referrals typically cost a fraction of paid advertising while delivering higher-quality customers

- Network effects: Payment apps and banking platforms become more valuable as more people join, making each referral a multiplier

- Built-in qualification: Advocates tend to refer people similar to themselves, which often means higher-value customers with better credit profiles and engagement patterns

- Organic reach: Referrals extend marketing into networks that would otherwise be inaccessible via paid channels

PayPal famously spent $60-70 million on referral bonuses during its early growth phase, but the cost per acquired customer was still lower than traditional marketing. More importantly, those referred customers stuck around longer, referring more customers and becoming a self-sustaining growth engine.

Top 10 fintech referral program examples

These innovative fintech brands each took a different approach to referral program design, from straightforward cash bonuses to gamified experiences. Each one offers lessons for financial services teams building their own programs—what to reward, which incentives work best, and the personalized touches that made their programs stand out.

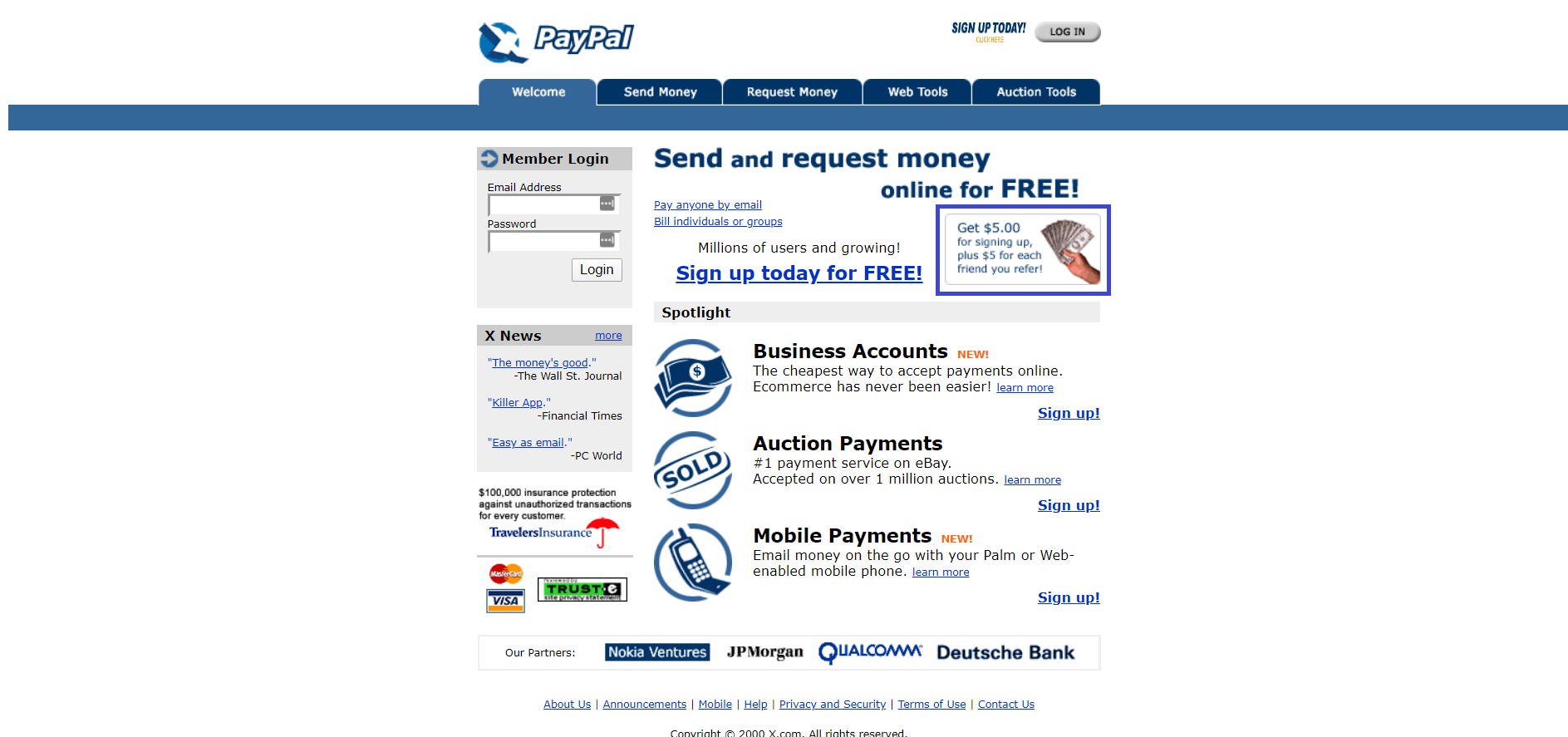

1. PayPal and the original double-sided referral

PayPal essentially invented the modern fintech referral playbook. In its early days, the company offered $20 to both the advocate and the referred friend—a structure that helped PayPal grow from 1 million to 5 million users in just a few months. The genius was in the simplicity: cash rewards appeared directly in your PayPal balance, ready to spend.

The double-sided model became the template for nearly every fintech referral program that followed. By rewarding both parties, PayPal created a sense of fairness that encouraged sharing without feeling transactional. The referral incentive also encouraged advocates and new users to keep engaging with the product—they had cash to spend!

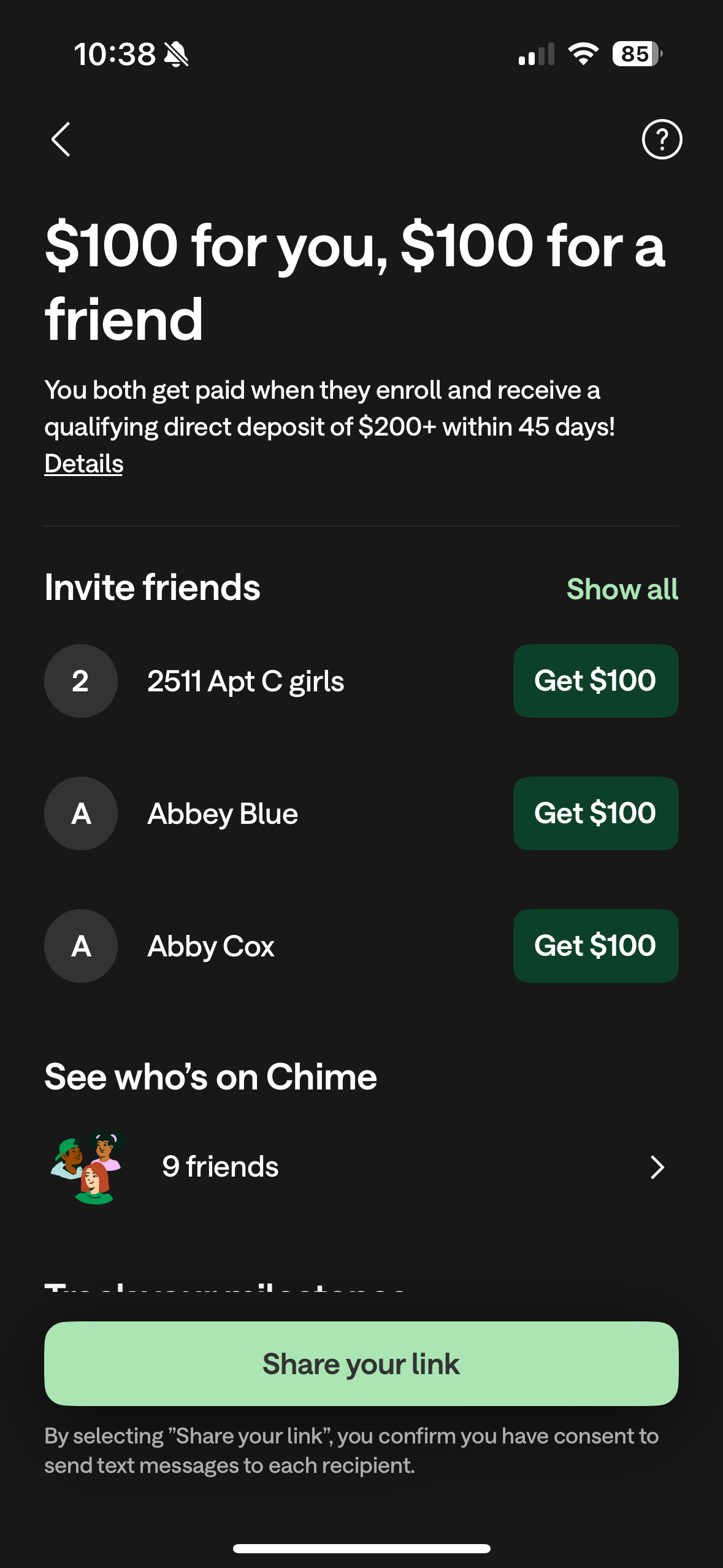

2. Chime and high-value cash bonuses

Chime’s referral program takes a direct approach with high-value cash rewards—$100 for both the advocate and their referred friend. The reward value is particularly critical here given the higher qualification barrier: customers have to set up and receive a qualifying direct deposit in their new account, an action that requires a high level of trust from the user. The reward then deposits automatically into the user’s Chime account, reinforcing the product experience.

What makes Chime’s program effective is its visibility. The referral option appears prominently in the app, with CTAs appearing at several user touchpoints. The ease of sharing plus the advertised reward value gives users a genuine reason to refer. For mobile banking apps competing on features that often look similar, a generous referral bonus can be a real differentiator.

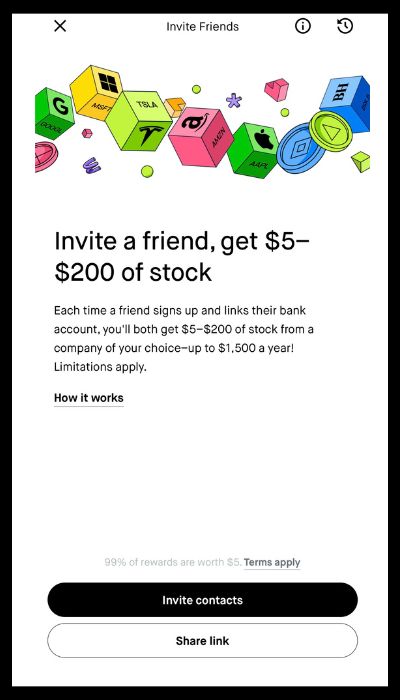

3. Robinhood and gamified stock rewards

Robinhood brought gamification to fintech referrals by offering free stocks instead of cash. When you refer a friend, both of you receive a randomly selected stock—revealed through a virtual scratch-off card. The stock could be worth anywhere from a few dollars to several hundred, adding an element of excitement to the experience while tapping into what Robinhood users value—investment opportunities.

The approach does two things well: It makes the referral feel like a gift rather than a transaction, and it encourages new users to engage with the core product immediately. You can’t help but check what stock you received and watch how it performs.

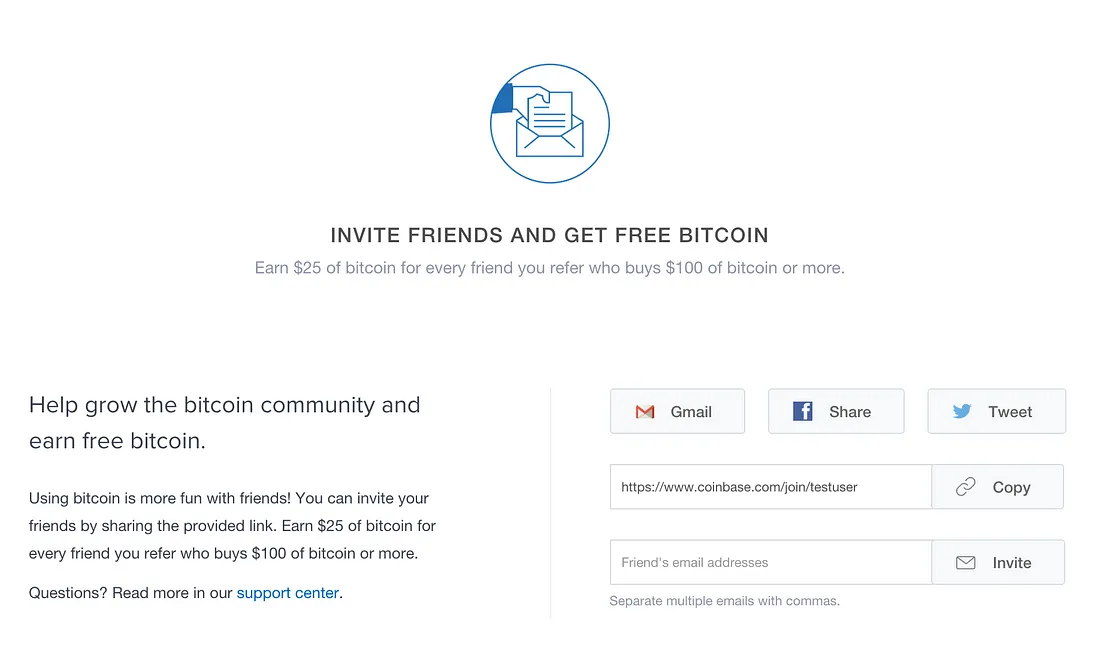

4. Coinbase and personalized crypto incentives

Coinbase rewards referrals with cryptocurrency—typically $10 in Bitcoin for both parties after the new user completes their first trade. The reward aligns perfectly with the product itself, essentially giving new users their first taste of crypto ownership without any risk.

For crypto platforms, this approach serves as both acquisition and education. New users who receive Bitcoin as a reward are more likely to explore the platform, learn about other cryptocurrencies, and eventually make their own purchases.

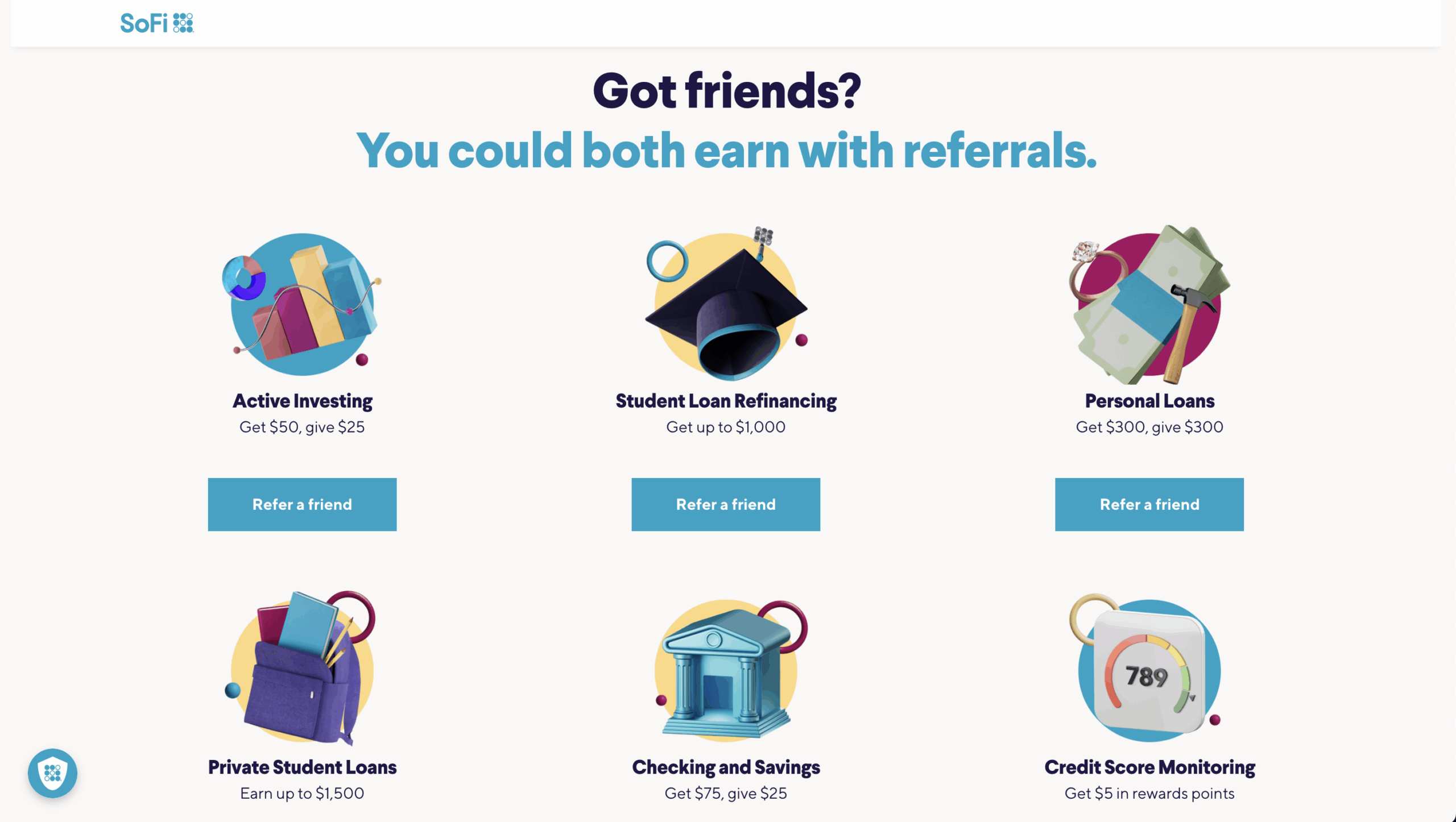

5. SoFi and tiered rewards across products

SoFi operates across multiple financial products—loans, investing, banking, credit cards—and its referral program reflects that complexity. Reward amounts vary based on which product the referred friend signs up for, with higher-value products like mortgages earning larger bonuses.

The tiered structure makes sense for multi-product fintechs. A checking account and a mortgage represent very different customer values, so the referral incentives scale accordingly. SoFi prominently displays lifetime referral earnings in the app, which has reportedly exceeded $20 million paid to members.

6. Wealthfront and the investment referral program model

Wealthfront takes a product-based approach to referral rewards. Instead of cash, both parties receive a certain amount of assets managed without fees. This structure is common among robo-advisors and investment platforms, where the value proposition centers on low-cost investing.

The fee waiver reward reinforces Wealthfront’s core message about minimizing costs. It also creates an ongoing relationship—the referred customer continues to benefit from the reward as long as they maintain their account.

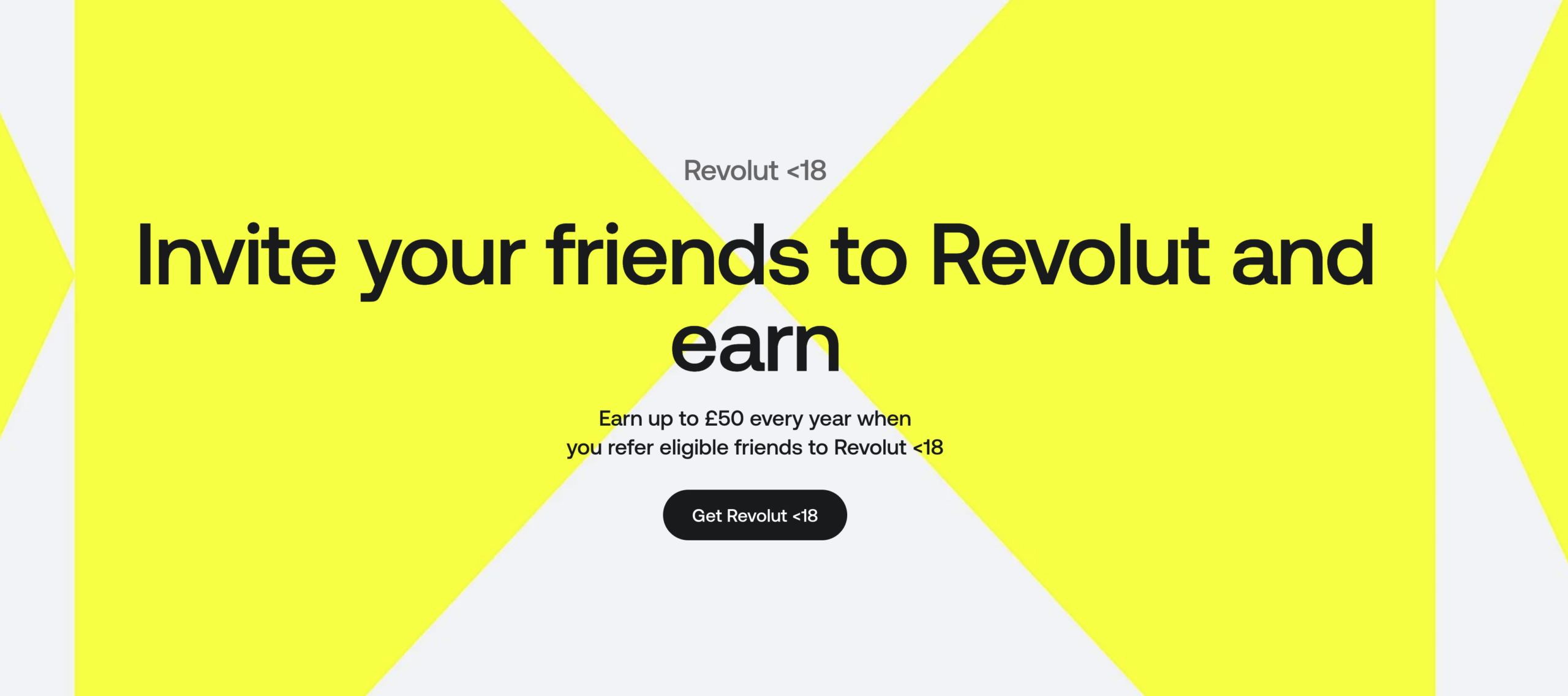

7. Revolut and youth account referrals

Revolut leverages referral rewards to tap into a valuable growth channel that many fintechs struggle to reach: teen and youth accounts. Both Gen Alpha and Gen Z are eager to learn about finance and investing, but most platforms don’t cater to that demographic. Fintech innovator Revolut bucked that trend with its dedicated youth accounts, Revolut <18. Its referral program offers rewards of up to £50 to teens who invite their friends to join the platform—encouraging more young people to develop smart money habits early.

The program is easy to use, making it perfect for teens opening their first-ever bank accounts. Rewards get deposited automatically, so there’s no digging through complicated qualification steps—just the excitement of cash in the bank.

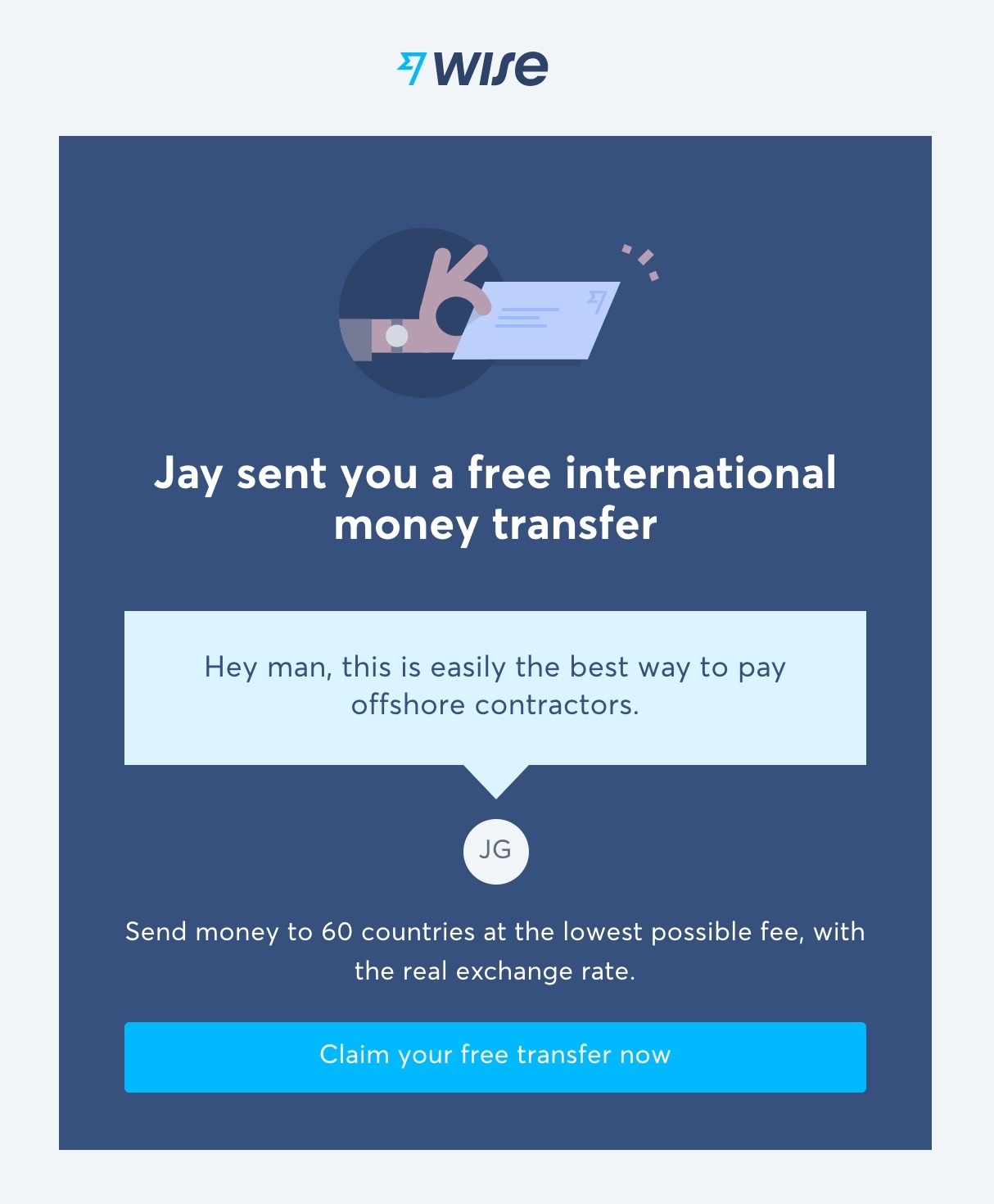

8. Wise and trust-building transparent rewards

Wise (formerly TransferWise) emphasizes clarity in its referral program, which fits a company built on transparent pricing. The terms are straightforward: invite friends, and both of you receive a bonus after they complete a qualifying transfer.

For international money transfer services, trust is paramount. Wise’s referral program reflects the same no-hidden-fees philosophy that defines its core product, which helps convert skeptical first-time users.

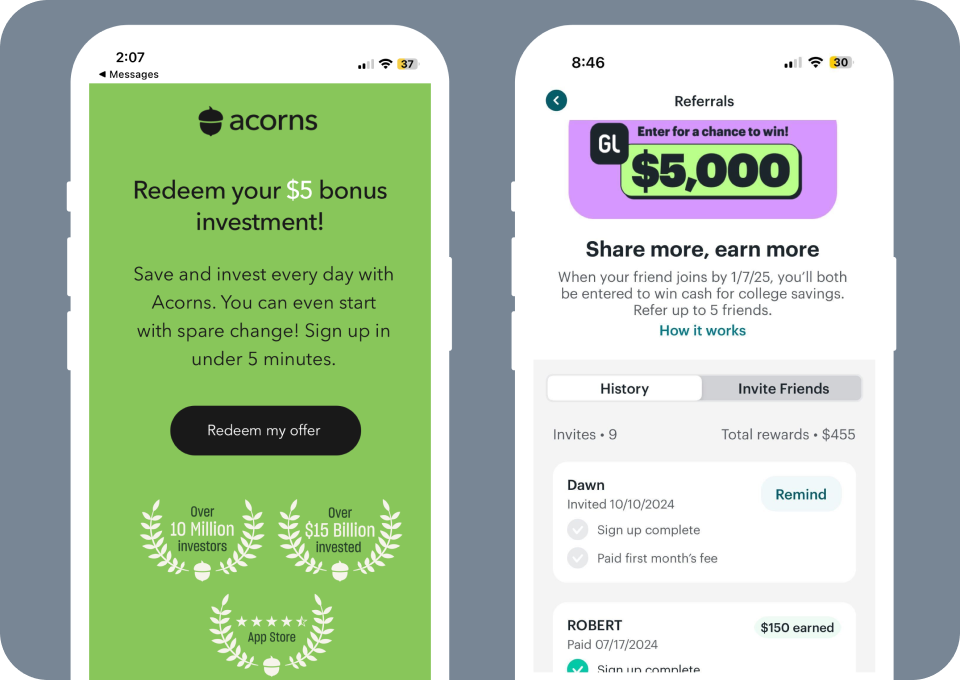

9. Acorns and micro-investing referral bonuses

Acorns offers modest cash bonuses—typically $5—that deposit directly into the user’s investment account. While the amount is smaller than some competitors, it aligns perfectly with Acorns’ micro-investing model, where users invest spare change from everyday purchases.

The approach particularly resonates with younger users and first-time investors who are starting small. A $5 bonus feels meaningful when your account balance might only be $50.

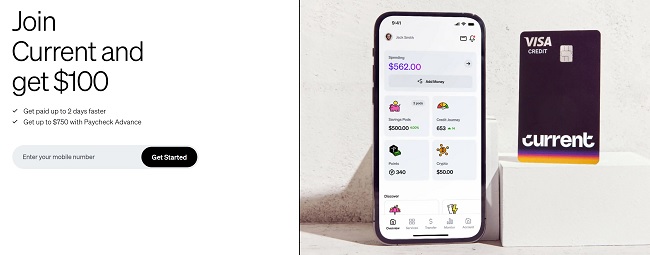

10. Current and Gen Z-focused mobile referrals

Current has designed its referral program specifically for Gen Z users, with mobile-first sharing that integrates naturally with social platforms. The experience feels native to how younger users already communicate—quick, visual, and shareable.

The program emphasizes speed and simplicity, with rewards that process quickly and clear progress tracking. For a demographic that expects instant everything, that responsiveness matters.

| Company | Reward Type | Double-Sided | Best For |

|---|---|---|---|

| PayPal | Cash | Yes | Payment apps |

| Chime | Cash | Yes | Mobile banking |

| Robinhood | Free stock | Yes | Trading platforms |

| Coinbase | Crypto | Yes | Crypto exchanges |

| SoFi | Tiered cash | Yes | Multi-product fintechs |

| Wealthfront | Fee-free management | Yes | Investment platforms |

| Revolut | Cash | Yes | International banking |

| Wise | Cash | Yes | Money transfers |

| Acorns | Cash | Yes | Micro-investing |

| Current | Cash | Yes | Gen Z banking |

Best practices for building a finserv referral program

The most successful programs share common elements that drive participation and conversion. Here’s what consistently works across the financial services industry.

Keep the offer simple and transparent

Complex terms kill referral programs. If users have to read all the fine print to understand whether they’ll actually receive a reward, many won’t bother sharing at all. The best programs communicate the offer in a single sentence: “Give $50, Get $50” or “You both get a free stock.”

Transparency also means being clear about qualifying conditions. If the referred friend needs to make a minimum deposit or complete a specific action, it builds trust to state that upfront rather than burying it in terms and conditions.

Personalize your rewards to your audience

Cash works for most audiences, but it’s not always the most effective choice. Younger users might respond better to gamified rewards or product credits, while high-net-worth customers might prefer fee waivers or premium service upgrades.

The key is matching incentives to what your specific users actually value. A platform focused on crypto enthusiasts will likely see better results offering Bitcoin rewards than cash, even if the dollar value is identical.

Use double-sided incentives for advocate and friend

Over 78% of referral programs reward both parties. The structure feels fair—the advocate isn’t just extracting value from their friends, they’re sharing something genuinely beneficial. That psychological shift makes people more comfortable sharing and makes referred friends more likely to convert.

The balance between advocate and friend rewards can vary. Some programs weight rewards toward the advocate to encourage more sharing; others emphasize the friend’s reward to improve conversion rates. Testing different ratios helps identify what works for your specific audience. A tiered program that gives bonuses to frequent advocates—with or without raising the friend reward—is another incentive structure to consider.

Embed referrals in your mobile banking experience

Placement matters enormously. Programs buried in settings menus generate far fewer referrals than programs featured prominently on the home screen or during high-engagement moments like after a successful transaction.

The most effective implementations let users share directly from the app—generating a unique link, sending it via their preferred messaging platform, and tracking results without ever leaving the banking experience. Extole integrates with digital banking platforms like Banno, Q2, Alakmi, and Candescent to enable exactly this kind of seamless embedding.

Automate reward fulfillment and events tracking at scale

Manual reward processing breaks down quickly as programs grow. Automated systems handle verification, fraud detection, and reward distribution without human intervention—which means faster fulfillment and happier customers.

Equally important is the tracking infrastructure. Understanding which advocates drive the most valuable referrals, which channels perform best, and where drop-off occurs in the referral funnel requires robust event tracking and analytics.

Optimize performance with A/B testing and analytics

The first version of any referral program is rarely the best version. Continuous testing—different reward amounts, messaging variations, placement options, and timing—reveals what actually drives results for your specific audience.

Key metrics to track include referral share rate (how many customers share), conversion rate (how many shared links result in new accounts), and referred customer quality (lifetime value, engagement, retention).

Fintech alternatives to traditional cash rewards

While cash remains the most common referral incentive, several alternatives can be equally or more effective depending on your audience and product:

- Points and bankable rewards: Customers earn redeemable points for referrals alongside other engagement actions, creating a unified loyalty ecosystem

- Product-based rewards: Free trades, fee waivers, or bonus investment amounts that reinforce the core product experience

- Tiered and gamified rewards: Variable rewards based on referral volume or random selection that add excitement and encourage continued participation

- Charitable donations: Options to donate reward value to causes, which appeals to socially conscious users

The best fintech rewards programs often combine referral incentives with points earned for other actions—completing profile information, setting up direct deposit, or reaching savings goals. The approach turns referrals into one component of a broader engagement strategy rather than a standalone program.

How to launch a scalable financial services referral program

Building a referral program that scales requires thoughtful planning across several dimensions. Here’s a framework that works for most financial services organizations:

- Define your goals: Set specific targets for customer acquisition volume, cost per acquisition, and customer quality metrics before launching

- Design your incentive structure: Choose reward types and amounts for both advocates and referred friends based on customer lifetime value and competitive positioning

- Build or select your platform: Evaluate whether to build in-house or use an enterprise referral platform that provides integrations, fraud protection, and analytics out of the box

- Integrate with existing systems: Connect the referral program to your CRM, banking core, and marketing automation tools for seamless data flow and personalization

- Launch and promote: Announce the program through email, in-app messaging, and other channels—and continue promoting it at key moments in the customer journey

- Monitor and optimize: Track performance metrics, run A/B tests, and iterate on rewards, messaging, and placement based on results

Enterprise platforms like Extole provide pre-built templates, compliance features, and integrations with leading digital banking solutions that can significantly accelerate this process without sacrificing quality and compliance.

Book a demo to see how Extole helps banks and fintechs launch referral programs that scale.

FAQs about financial services referral programs

Why are referred customers more valuable in financial services?

Referred customers arrive with built-in trust because someone they know personally vouched for the institution. That trust translates into higher engagement from day one, stronger retention over time, and greater willingness to try additional products.

What is the ideal reward value for a fintech referral program?

The right reward value depends on your customer lifetime value and acquisition cost targets. Most fintechs test multiple reward levels to find the sweet spot—high enough to motivate sharing but not so high that it attracts low-quality referrals or erodes unit economics.

How do investment referral programs differ from banking referral programs?

Investment platforms often use product-based rewards like free trades, managed assets without fees, or bonus contributions rather than direct cash. Banking referral programs typically offer cash bonuses deposited directly into accounts, which aligns with the core value proposition of easy access to money.

What fraud prevention measures protect finserv referral programs?

Effective programs use multiple layers of protection: identity verification to confirm real people, velocity checks to catch unusual referral patterns, device fingerprinting to identify repeat devices, and rules-based systems to detect self-referrals and coordinated abuse.

How do financial services teams measure referral program ROI?

The core metrics include referral share rate (percentage of customers who share), conversion rate (percentage of shares that become customers), cost per acquired customer, and referred customer lifetime value compared to other acquisition channels.

Can fintech companies run effective referral programs without cash rewards?

Yes. Many fintechs successfully use points, product credits, fee waivers, or gamified rewards—especially when those incentives align naturally with the product experience. A trading platform offering free stocks or a robo-advisor offering fee-free management can be more compelling than cash because the reward reinforces the core value proposition.